Blockchain is one of the most revolutionary technologies of modern times, fundamentally changing approaches to data storage and transmission. Its capabilities are widely applied across a variety of sectors, from finance and cryptocurrencies to healthcare and government. However, despite the fact that blockchain is a term that became widely known through cryptocurrencies, its potential goes far beyond them.

Blockchain technology was proposed in 2008 under the pseudonym Satoshi Nakamoto, who created the first decentralized cryptocurrency—Bitcoin. In his original approach, Nakamoto introduced the concept of a distributed ledger in which transactions are recorded in a chain of blocks, secured by cryptography. This mechanism became the foundation for the first functioning blockchain system. In 2009, the first block was mined, marking the beginning of the cryptocurrency era.

With the development of blockchain technology, many new applications emerged. In 2013, the Ethereum project was launched, opening new horizons by proposing the use of smart contracts to automate and verify transactions without intermediaries. Blockchain is an innovative system that continues to evolve, with its implementation covering an increasing number of industries.

In this article, we will explore what blockchain is, how it works, its main advantages, and the challenges it faces. Dive into the world of the technology that is shaping our future!

Blockchain: Basics and Principles of Operation

Blockchain (from English blockchain, “block chain”) is a new form of distributed database that stores information in the form of a continuous chain of blocks. Each block contains records of transactions and is linked to the previous block using cryptographic methods, ensuring data security and immutability.

What is Blockchain?

Blockchain is a distributed ledger that is decentralized and does not require central management. Data in the blockchain is recorded chronologically, forming a protected chain of blocks. This structure provides several key advantages:

- Reliability: Any changes to the ledger must be approved by network participants.

- Transparency: All data is accessible for viewing by registered users.

- Security: The use of cryptography makes data falsification nearly impossible.

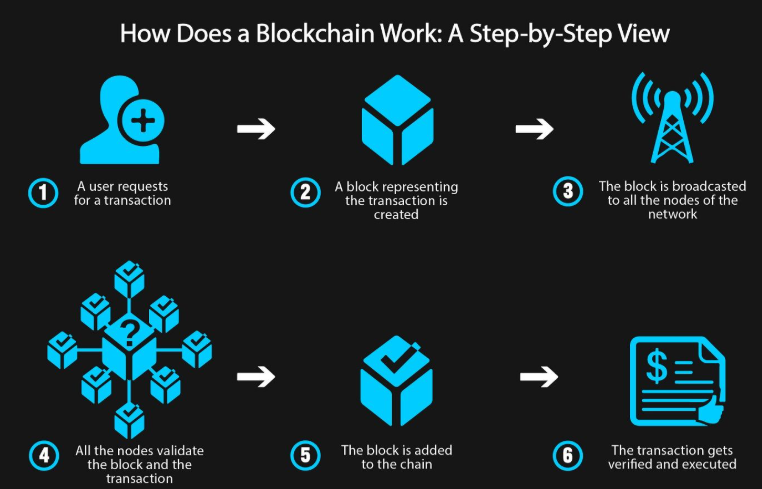

How Blockchain Works:

- Transaction Creation: A user sends data to the network. This could be a financial operation, information transfer, or confirmation of some action.

- Block Formation: Multiple transactions are grouped into a block.

- Block Verification: The network participants use consensus algorithms such as Proof of Work or Proof of Stake to verify the accuracy of the data.

- Block Addition to the Chain: After verification, the new block is added to the existing chain, creating a continuous record of data.

- Copy Update: All nodes in the network receive the updated version of the blockchain.

Key Components of Blockchain:

- Block: Contains transaction information, the hash of the current block, and the hash of the previous block that links the blocks together.

- Blockchain: A sequence of blocks organized into an immutable structure.

- Nodes: Computers or devices that maintain and synchronize the blockchain copy.

- Consensus Algorithms: Mechanisms that ensure agreement between network participants.

How Do These Structures Ensure Data Security in Blockchain?

Each block in the blockchain retains data about transactions conducted during a specific time period, and through cryptographic methods, forms a secure and reliable chain, creating an immutable and publicly accessible distributed ledger. Simply put, blockchain is a ledger that includes all historical transactions. Every node in the network stores its copy of this ledger, and through consensus algorithms, data consistency is maintained across all nodes. Each block can be viewed as a page in a ledger that records transactions made during a certain period. Thus, all transaction details are recorded in a public ledger, accessible to all participants, and altering an already recorded transaction requires simultaneous changes to data across all nodes in the network that store this ledger. Furthermore, because each page of the blockchain contains a hash of the previous page, altering data in one block (i.e., falsifying a transaction) would cause a mismatch in the hash with the subsequent block. This would require changing the data in the next block, and so on, in the chain. Thus, modifying information in one block would necessitate a review of all subsequent blocks, and considering that these changes must be agreed upon by all network participants, this becomes practically impossible. This is why blockchain has the property of immutability.

Blockchain has become the foundation for cryptocurrencies like Bitcoin, but its application extends far beyond the financial sector. This technology enables trust and transparency in many fields, including logistics, healthcare, government, and more.

Advantages of Blockchain

Blockchain technology has gained widespread adoption due to its unique advantages. It opens new opportunities for enhancing security, efficiency, and transparency in processes across various sectors. Let's examine the key benefits of blockchain.

1.Decentralization

One of the main advantages of blockchain is its decentralized structure. Unlike traditional centralized systems, blockchain does not have a single governing entity or server. Instead, all data is stored and verified by multiple nodes in the network. This enables:

- Elimination of dependence on a single center.

- Increased system resilience against failures and attacks.

- Autonomous network operation.

2.Transparency

Blockchain provides a high level of transparency, as all data in the network is open and accessible for verification by all participants. This is particularly important for sectors such as finance, government, and logistics, where ensuring fairness and reliability is crucial. Example: In blockchain, the entire journey of a product can be tracked from the manufacturer to the end customer, minimizing the risk of counterfeiting and fraud.

However, not all blockchain systems operate with full transparency. Some of them implement privacy protection mechanisms to hide certain data or limit access to it. These measures are particularly needed when blockchain blocks contain personal data, trade secrets, or other sensitive information.

Example: Systems using Zero-Knowledge Proof technology allow the authenticity of a transaction to be verified without revealing its details. This combines blockchain's transparency advantages with the need for privacy.

3.Security

Blockchain's use of cryptographic algorithms makes it one of the most secure technologies. Each transaction is signed with a unique digital key and verified by all network participants. Falsifying or altering data retroactively is practically impossible due to:

- The connection of blocks through hash codes.

- Consensus mechanisms that prevent the addition of false data.

4.Immutability of Data

Data recorded in blockchain becomes immutable. This ensures:

- Long-term data storage.

- No possibility to delete or falsify records.

Blockchain's immutability makes it ideal for storing important data, such as medical records, legal contracts, and financial transactions.

5.Efficiency and Automation

Blockchain can automate many processes, especially using smart contracts. These programs automatically execute when pre-established conditions are met, which allows:

- Reducing costs for intermediaries.

- Speeding up operations.

- Minimizing human error.

Example: In logistics, smart contracts enable automatic payments for deliveries when goods are received.

6.Global Access and Inclusiveness

Blockchain networks are accessible to anyone with internet access. This is especially important in developing countries, where people often lack access to traditional financial services.

Due to these benefits, blockchain is becoming an indispensable tool for solving complex problems in the modern world. However, its implementation faces certain challenges, which will be discussed in later parts of the article.

Misconceptions About Blockchain

Misconception 1: Blockchain = Bitcoin Speculation

The explosive growth of Bitcoin in 2017 attracted investors who saw opportunities for profit in this new market. This led to the first misconception about blockchain: that blockchain is just a tool for cryptocurrency speculation.

However, Bitcoin is only one application of blockchain technology, much like Alipay is a product of internet finance. Today, digital currencies such as Bitcoin, Ethereum, Ripple, and others are traded, similar to stocks on traditional financial markets.

Moreover, tech giants like BATJ are actively exploring blockchain applications, already implementing it in fields such as product tracking, electronic evidence, and charity, helping society recognize the benefits of this technology.

Misconception 2: Data on the Blockchain is Completely Secure

Many, including experienced cryptocurrency market participants, believe that the data on the blockchain is encrypted and completely secure, so it’s safe to store sensitive information like bank accounts and passwords on the blockchain.

However, "absolute security" does not exist.In public blockchains, data is accessible to all nodes and participants in the network, meaning anyone can view this data.When people talk about "data security" in blockchain, they mean that the data cannot be modified—no one has the right to alter it. Therefore, blockchain is not suitable for storing private confidential information.

Misconception 3: Blockchain is Suitable for Storing Large Volumes of Data

The distributed nature of blockchain means that each node in the network holds a full copy of the entire blockchain. Using blockchain to store large files, such as videos, would create significant challenges for the nodes and reduce efficiency. For example, each block in the Bitcoin network can contain only 1 MB of data.

In such cases, large files are typically stored elsewhere, while only their "fingerprints" (hash values) are stored on the blockchain.

Misconception 4: Smart Contracts are Real Contracts Stored on the Blockchain

In reality, smart contracts are not traditional contracts. A smart contract is a computer program that can be stored on the blockchain, written in advance, and ready to execute.

Smart contracts are written in programming languages like Solidity for Ethereum, and with the Ethereum Virtual Machine (EVM), they can run on the Ethereum blockchain, expanding its functionality.

Bitcoin, as cryptocurrency 1.0, does not support smart contracts and cannot be used to create DApp applications, but it does support simple scripts to extend basic functionalities.

Thus, smart contracts are programs that automatically execute when predefined conditions are met, but only within the blockchain, and these conditions must be verifiable via blockchain technology.

Misconception 5: Bitcoin is the Same as Coins

Bitcoin is the first digital currency based on blockchain technology. In the real world, it does not have a physical form; it exists only as a transaction record in the blockchain.

Coins serve one function—to be a simple store of value—while tokens can store complex values, such as properties, utility, income, and fungibility, which makes them fundamentally different.

To buy, send, or receive Bitcoin, you only need a wallet, which is simply an address and a key, and the transaction itself is a valid record in the blockchain, verified by the nodes.

For example, when a miner receives 12.5 Bitcoin as a reward, this amount is simply a record of a transfer to the miner's wallet and does not exist in physical form.

Misconception 6: Bitcoin Won't Become a Primary Currency Due to Government

The main issue with Bitcoin is its scalability. According to Satoshi Nakamoto's design, creating a block in the Bitcoin blockchain takes about 10 minutes, and the block size is limited to 1 MB. This means Bitcoin can only handle 7 transactions per second. This speed makes Bitcoin suitable for transferring funds, but not for quick transaction confirmations.

Ethereum, as cryptocurrency 2.0, achieves only 20 transactions per second. Meanwhile, for example, during the 2017 "11.11 Shopping Day," Alipay processed over 256,000 transactions per second, and Visa and PayPal can handle far more transactions than Bitcoin and Ethereum.

Thus, the main reason Bitcoin cannot become a primary currency is its limited scalability, not government or regulatory restrictions.

Misconception 7: Blockchain Can Be Applied in Every Industry

Some view blockchain as a technology that will become an integral part of many industries and believe it is as important as the industrial revolution or the next stage of the internet's evolution.

While blockchain is a significant technological advancement, it is not suitable for every industry. In the short term, this technology cannot be applied everywhere. Today, creating a blockchain project requires substantial costs, and there is a shortage of specialists in this field. Therefore, most projects will be focused on areas where they will provide the greatest return.

Furthermore, blockchain does not solve all social trust problems, and the question "Is a truly 'decentralized' solution really possible?" remains open. However, despite misconceptions and gradual development, blockchain is becoming increasingly powerful and better adapted to modern times.

Conclusion

In Conclusion, despite the existing myths and misunderstandings, blockchain continues to evolve as a technology with enormous potential for various industries. Many of the misconceptions, such as associating blockchain solely with cryptocurrencies or assuming complete data security, can be dispelled by understanding how this technology works. Blockchain truly offers unique opportunities to create transparent and secure systems, but its application must be understood in the context of real capabilities and limitations.

Blockchain technology remains at the forefront of innovation, and despite the challenges, it continues to attract the attention of researchers and large corporations. It is important to recognize that for successful blockchain implementation, many factors must be considered, including technical, economic, and legal aspects. In the coming years, we are likely to witness further development of blockchain applications that could significantly impact various aspects of our lives.

Web Proxy Tools

Web Proxy Tools Free Tools

Free Tools Cookie Plugin

Cookie Plugin UA Generator

UA Generator MAC Address Generator

MAC Address Generator IP Generator

IP Generator IP Address List

IP Address List 2FA Code Generator

2FA Code Generator World Clock

World Clock Anonymous Check

Anonymous Check WebRTC Leak Test

WebRTC Leak Test UUID Generator

UUID Generator Free Web Proxy Site

Free Web Proxy Site Proxy Checker

Proxy Checker FB Ad Checker

FB Ad Checker AI Web Scraping

AI Web Scraping Free SMM Tools

Free SMM Tools Twitter Shadowban Checker

Twitter Shadowban Checker Instagram Name Checker

Instagram Name Checker UTM Generator

UTM Generator Username Generator

Username Generator AI Hashtag Generator

AI Hashtag Generator LinkedIn Headline Generator

LinkedIn Headline Generator Social Media Image Resizer

Social Media Image Resizer